Blockchain technology has the potential to enhance performance and operational efficiency, impacting businesses in multifold industries worldwide.

The business world is perpetually changing with new trends and technologies. Sometimes, it’s technologies like IoT and AI that help transform the sphere of business by automating operational workflows. At other times, there is cloud computing, efficiently managing and processing a huge pile of data in no time.

Amidst the ever-evolving technological landscape, another disruptive force has emerged with the capacity to reshape global businesses – Blockchain. This distributed ledger technology (DLT) has successfully navigated its way through numerous industries, catalyzing significant business transformations. The momentum it has amassed in recent years is formidable, and projections indicate a flourishing business value in the times ahead. Yet, the pivotal question remains: what is the true extent of its benefits for businesses on a global scale? As we delve into the potential of Blockchain, it’s worth noting the increasing relevance of blockchain app development services, reflecting the demand for tailored solutions in this transformative era.

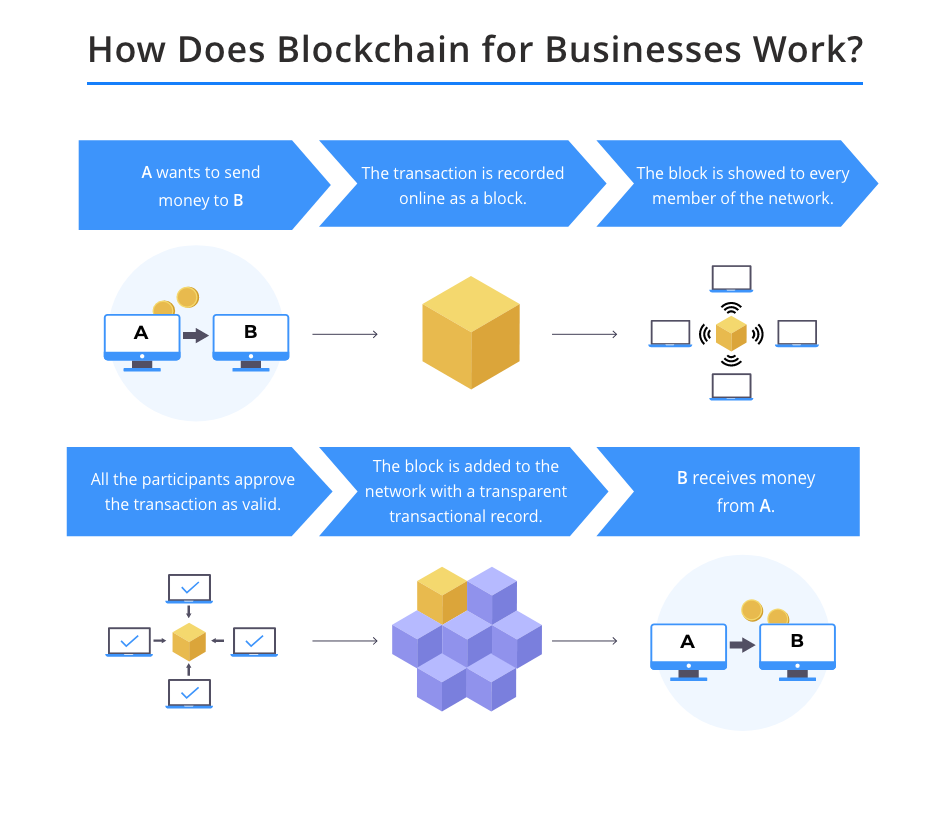

How Exactly Does Blockchain for Businesses Work?

Blockchain technology records and updates the digital information of who holds what in a ledger. By its very nature, the technology maintains a distributed database where a list of constantly growing records, known as blocks, are connected in the blockchain network.

Unlike centralized data management approaches, blockchain distributes copies of the ledger to all the participants available on the nodes. It makes each one of them participate in the consensus mechanism, making everyone a part of all the transactional updates on the ledger.

![Blockchain for Businesses]()

Blockchain for businesses can be an effective solution to improve operational efficiency, build relationships, and get real-time insights across the organization. Moreover, it enhances the chances of rapidly scaling up business growth. To deliver all these benefits, the following attributes of blockchain technology play a significant role:

Consensus

To update the shared ledgers, all the relevant participants belonging to a blockchain network must validate the specific transaction.

Immutability

One of the important characteristics of blockchain is data immutability. It means any record, once updated, can’t be changed, deleted, or tampered with. One can add more blocks to the chain, but can not remove the existing ones. This increases trust and strengthens bonds among stakeholders.

Replication

Once the participants approve the record of an event in a blockchain network, it automatically reflects across the ledgers for all members in it. In this way, every participant gets the same updated information in real time, leading to a ‘single trusted reality’ in terms of transactional records.

Security

Only authorized participants can create and access new blocks, especially when it comes to permissioned blockchains.

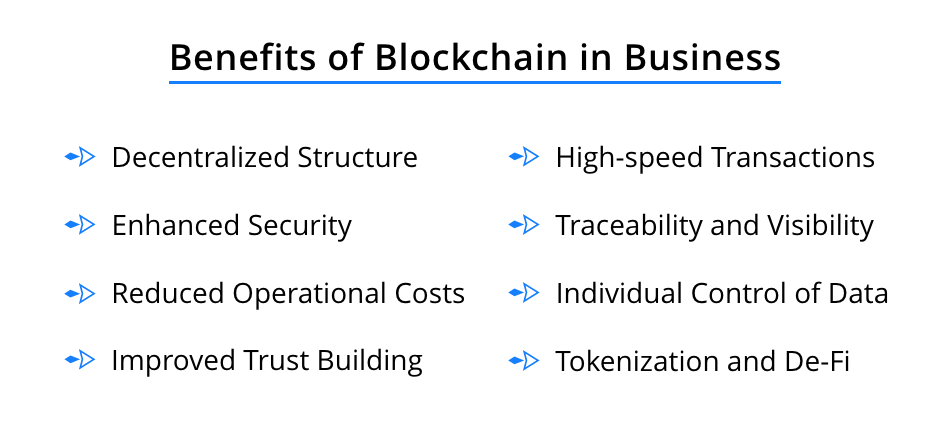

What Are the Benefits of Blockchain in Business?

The true value of blockchain for businesses stems from its capabilities to store and process data quickly and securely among the entities in the ledger. And the best part is, no one needs to take responsibility to safeguard or facilitate the transactions. Here are some top blockchain benefits for business:

![benefits of blockchain in business]()

Decentralized Structure

Blockchain can be an effective solution in a business structure where participants are unknown to each other. For instance, blockchain can help manage a supply chain network consisting of different entities – suppliers, retailers, distributors, transportation partners, etc. All these participants can easily access information without worrying about taking authorization from any centralized authority.

Improved Security

The security aspect of blockchain could be understood by the fact of how this technology operates. By creating tamper-proof digital records added with end-to-end encryption, businesses can stay carefree in terms of unauthorized access and activities. Moreover, with data anonymization, blockchain can easily address the privacy concerns of the participants of the business.

Cost Reduction

One of the significant benefits of blockchain for businesses is that it reduces operational costs. By making transactional processes efficient, it minimizes manual tasks like data collection, reporting, and auditing. Experts believe that organizations, especially financial institutions can make great savings using blockchain through its capabilities and eliminating middlemen and third-party providers.

Trust Building

Blockchain’s nature of transparency creates and strengthens business relationships among different participants in the network where trust building seems non-existent. That’s what makes these entities engage in business dealings that might not otherwise be involved without a reliable intermediary.

High-speed Transactions

By replacing manual tasks with automated functions and removing intermediaries, blockchain manages and processes transactions relatively faster than conventional methods. In fact, in some cases, blockchain-based transactions could take not more than a few seconds to process.

However, the processing time could vary based on how massive each block of data and traffic on the network is.

Traceability and Visibility

With blockchain, companies can easily trace the origin of the products and manage inventory. They can also track defective products and replace them with good ones. The case study of Walmart using blockchain for food traceability can be a great example here. The team that took around seven days to trace a package of sliced mangoes got it done in 2.2 seconds using a blockchain-based Hyperledger Fabric system.

Individual Control of Data

One of the best things about leveraging blockchain for businesses is that you get an incomparable level of individual control and privacy over data. Organizations can easily decide what piece of information they want to share, with whom, and for what time.

Tokenization and De-Fi

Transferring capital and lending money around the globe becomes easy with decentralized finance (DeFi) apps and tokenization – other important applications of blockchain technology. Using tokenization, one can easily convert the value of their assets into a digital token recorded and shared on a blockchain network. With DeFi, the role of centralized authorities and intermediaries could be eliminated, allowing businesses to conduct financial transactions quickly and securely.

What Is the Impact of Blockchain on Business in Different Industries?

Several industries are finding blockchain better than the existing approaches they rely on for performing crucial business operations. Below are the major sectors that blockchain can disrupt significantly.

Banking and Financial Industry

Over 91% of banks and financial institutions have already invested in blockchain solutions. Why? Well, the conventional methods include huge paperwork and time-consuming processes. They not only lead to high friction and delays but also lower the operational efficiencies of organizations across the industry.

By using blockchain, a wave of transformation is observed in the financial sector. Improvements were observed in the areas of global trade and consumer banking. Besides this, blockchain-based solutions also help in removing long-standing friction and automating compliance processes aligning with immutable records.

On an individual level, blockchain relies on a peer-to-peer approach, ensuring low fees and high security. Organizations can easily make a transaction using cryptocurrency, eliminating the need for third-party to transfer funds. Also, since every transaction is recorded in the ledger, one can quickly review it, offering true autonomy over the transactions made.

Healthcare Industry

The healthcare industry is one of those sectors that have mostly been unsettled by data breaches. Besides this, since an enormous amount of data is generated daily, managing it becomes extremely hectic and cumbersome.

However, by using blockchain in healthcare, storing, managing, and sharing patients’ records becomes effortless, while keeping their security intact. The technology has already demonstrated its significance by offering trust and collaboration to the patients, enabling them to have complete control over their private information.

Moreover, with the traceability characteristic of blockchain technology followed by supply chain management protocols, one can also distinguish and separate counterfeit medications from genuine ones.

Food and Supply Chain Industry

What makes a supply chain stronger and more resilient? Well, it needs streamlined operations, end-to-end visibility, and trust between trading partners to make it happen. Thanks to blockchain, all of this is possible now, enhancing the relationship among the participants in a specific supply chain.

When it comes to the food industry, blockchain technology for business can help ensure that food is safe and fresh. Furthermore, to deal with contamination, blockchain-based systems can be integrated to trace the food back to its source in a few seconds, which used to take days.

Insurance Industry

The use cases of blockchain in business can be also observed in the insurance sector. Companies are leveraging smart contracts to streamline and automate time-consuming processes like claims processing and settlement, underwriting, etc.

Besides this, by integrating other advanced technologies such as AI and RPA into the insurance industry, businesses can enhance operational productivity and reduce expenses. Blockchain can also streamline shared processes, further leading to workflow automation and minimizing disputes.

Government Sector

Blockchain has also proved to be beneficial in the government sector. Using this technology, an organization can easily and legally transmit the personal identification of individuals through electronic mediums. Also, acquiring and verifying passports, preparing legal documents, and filing regulatory forms, such as mortgage deeds become convenient.

Besides this, one of the best things about using blockchain for business in the government sector is eliminating voter fraud. In a conventional process, voters used to stand in lines or cast their votes by mail. These votes were counted by some local authority, and the presence of a central body can raise the chances of fraud.

However, by using blockchain technology, individuals can cast their votes without revealing their identities. These votes are registered in the form of digital IDs and each ID reflects only one vote. Once an ID is entered into the ledger, it cannot be erased or altered, making the occurrence of fraud almost impossible.

MiVote can be one of the popular examples of blockchain applications in the government sector. It is a token-based platform where voters can cast their votes through their mobile devices. These votes are registered into the ledger, making the process safe and reliable.

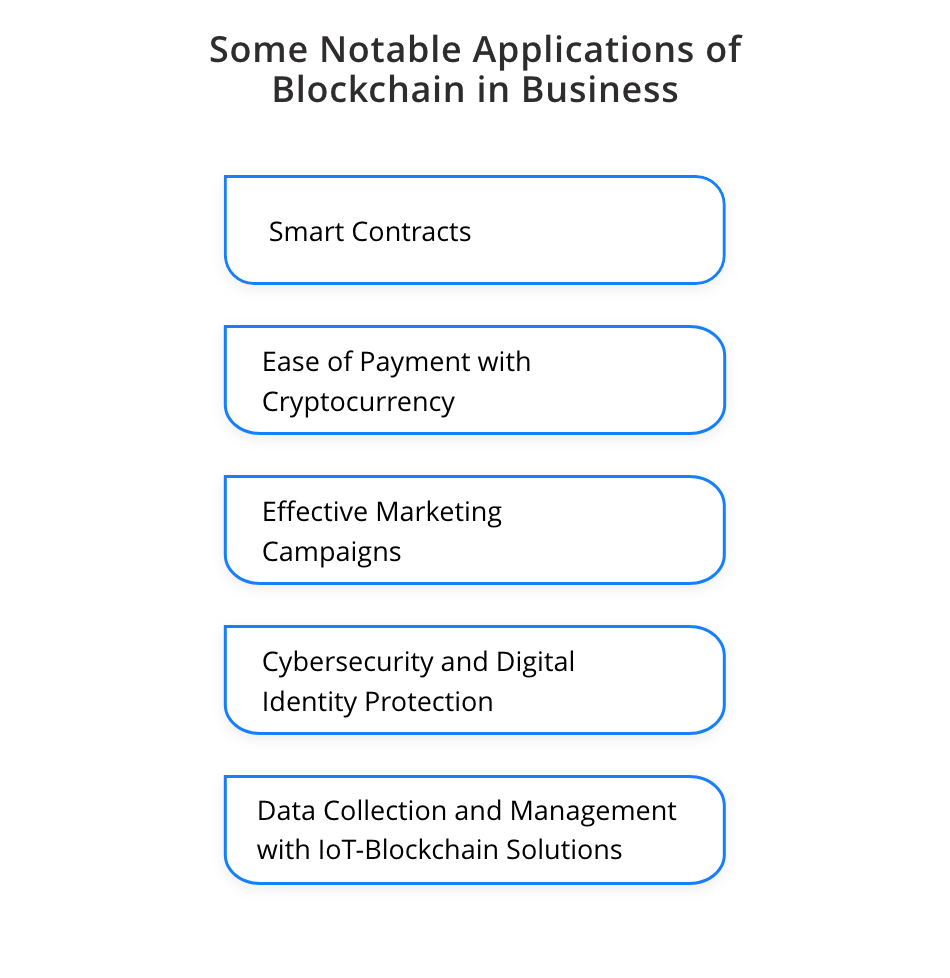

What Are Some Prominent Blockchain Applications for Businesses?

There are various blockchain applications that help revamp existing business models and strengthen corporate relationships. Here are some of the most popular blockchain applications that lead businesses to the path of digital transformation.

![examples of blockchain applications]()

Smart Contracts

The most remarkable blockchain application for business is smart contracts. They can be defined as a program that follows a specific business logic to implement agreements and conduct transactions among the participants in a blockchain network. Using smart contracts, businesses can create and implement legal agreements without involving any centralized authority or third-party middlemen.

The terms and conditions of smart contracts are mentioned in the form of codes. Once these codes are formulated, they are stored in a blockchain ledger, making them immutable. Simply put, when the written code is fulfilled, the conditions associated with it execute. If somehow, any participant tries to overrule these conditions, the specific services are returned to another party in a blockchain.

Ease of Payment with Cryptocurrency

Today, several trends in the mobile payment domain leverage the power of blockchain technology to make transactions quick and convenient. By eliminating the need to involve third-party payment merchandise for documentation and billing, blockchain for businesses has eased the process of cash flow.

The emergence of different types of cryptocurrencies like Bitcoin and Ethereum has also transformed the face of the payment industry. This has also become prominent after high-profile companies like Microsoft, Tesla, and AT&T started accepting Bitcoin as a payment medium for some services. In fact, Tesla included cryptocurrency in their investment portfolios as well.

Effective Marketing Campaigns

Another use of blockchain in business is taking marketing campaigns and promotional activities to the next level. Blockchain business models used in marketing can form a more secure and trustable relationship between companies and their customers. Besides this, here are the ways through which blockchain can impact digital marketing campaigns and strategies to make more profits:

Compensating the Users for Viewing Ads

Advertisements have become a permanent part of nearly all the channels users access. Some users have no specific issues with them, but others get easily irritated by these never-ending ads. However, how good it could be if the advertising experience becomes worthwhile for both businesses and consumers?

Well, some companies have started enhancing the ad experience for the viewers by compensating them with some kind of digital currency or token. Brave, a browser program, that enables users to view their private ads to get compensated with gift cards or redeemable tokens can be a significant example here.

Complete Security of User’s Data

There are times when you might have got newsletters from companies you never subscribed to. This happens because some companies share or sell your data (even if it’s just your name or email address) to other enterprises.

Blockchain can be really helpful in this case, as the transactions made using this technology are completely anonymous. As a result, users do not have to worry about losing their data to others.

Transparent and Reliable Marketing

Consumers doubting brands when it comes to marketing campaigns is normal. Especially when they make such claims that they sell something 100% unique or organic.

However, blockchain can help brands by making their marketing campaigns more transparent. Since all the transactions and data are visible to all the participants in a blockchain, businesses can easily prove their supply chain and marketing processes.

Consequently, this makes it easier for consumers to perceive a brand and its marketing strategies as reliable. The role of blockchain for small businesses can be significant here, as it offers them a competitive advantage against big box stores.

Getting More Accurate Leads

Currently, businesses collect user data through cookies. However, it’s not like this data is always reliable, making some of the campaigns unsuccessful. To resolve this problem, companies can make the right use of blockchain in business as it extracts data directly from the users.

Since the data is handed over by the customers themselves, it will be more accurate to be used for efficient marketing. As a result, companies can get more genuine leads to go with.

![impact of blockchain on business]()

Cybersecurity and Digital Identity Protection

Digital identity protection (DIP) is another one of the most important use cases of blockchain in business. No matter how secure your business platform is, there is always a slight scope of your users’ data falling into the hands of unauthorized individuals. In fact, this mostly happens with startups that knowingly or unknowingly sign up for several free sites and tools in their initial phase. Some of such portals could be malicious and hack your data, using it for their own profits.

Using blockchain for business can help companies to protect themselves against such intruders and cyber attackers. Moreover, blockchain’s robust encryption mechanism and other cybersecurity strategies ensure the complete protection of participants’ data.

Robust Data Collection and Management with IOT-Blockchain Solutions

Companies can also make the best use of blockchain in business by integrating it with state-of-the-art technological solutions like IoT. It is one of the prominent blockchain technology trends that enables IoT devices to share data in a permissioned or private blockchain, making tamper-free records of the transactions. This helps in maintaining the integrity of data without any need for centralized authority and management.

Businesses across different industries can set up IoT devices and systems and connect them via the Internet to collect and record data. The data gathered from the sensors in IoT devices can be used for asset management, product traceability, and real-time insights, depending on the operational industry.

Moreover, these blockchain-based IoT-integrated applications can also promote business automation by automatically collecting and analyzing data to make informed decisions. For instance, in the mechanical sector, systems can track themselves when there are issues in a part of a semi-autonomous machine. The system can order a replacement part in order to maintain the workflow.

However, all this is possible only when your development team is well-versed in both blockchain and IoT technologies. They must be aware of the best blockchain programming languages and coding practices that complement the latest technological trends.

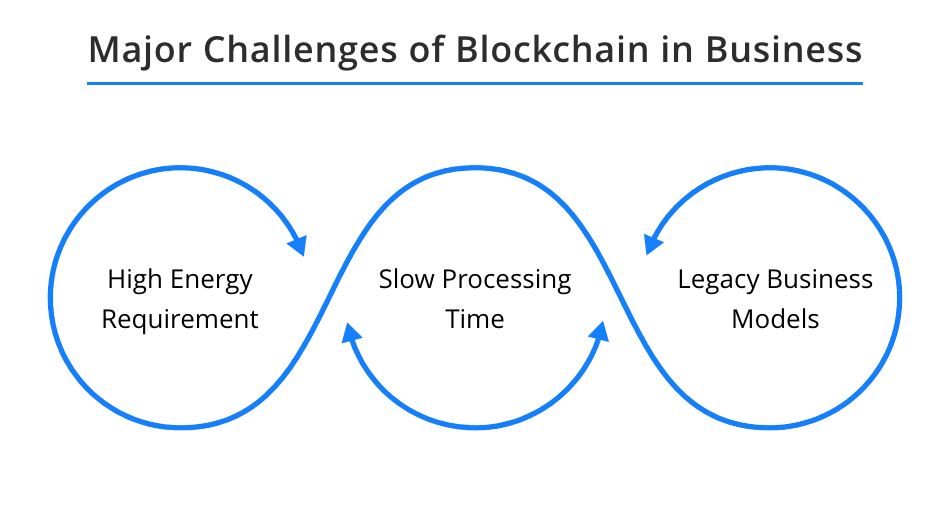

Challenges Companies Need to Overcome When Using Blockchain for Businesses

There is no doubt that blockchain has the right potential for businesses to thrive in the current industrial landscape. However, there are still a few issues that must be addressed before it goes mainstream in all sectors.

![challenges of blockchain in business]()

High Requirement of Energy

The process of verification of transactions is highly energy-intensive as high computational power is required to solve equations. Due to this, businesses would need a massive capital investment to harness and maintain the power used for these computational operations.

Slow Processing Time

All the complexities involved in the computations lead to delays in processing or make the overall process slow. However, experts and researchers are doing their best to figure out a better way that simplifies these calculations and makes processing faster than ever.

Legacy Business Models

One thing to keep in mind while using blockchain technology for business is that only those organizations having a DLT-based infrastructure can take advantage of it. Simply put, if you are operating with legacy systems, you can not leverage the benefits of blockchain for business transformation.

What is the Future of Blockchain for Businesses?

The ever-growing trends in blockchain technology are constantly disrupting the business world to a large extent. Its marketing potential is so high that researchers have projected the investment in blockchain solutions to reach $19 billion by 2024.

Many experts even believe that the true value of blockchain for businesses is observed in areas where conventional technologies and databases failed to flourish. Especially, when it comes to transparency and decentralization in operations, blockchain could be the best solution businesses can leverage.

Also, when paired with advanced technologies like artificial intelligence and machine learning, the decision-making process can be enhanced to an ultimate level. The combination may not only make the processing faster but also improve the efficiency of consensus.

Moreover, with cryptocurrency and tokenization entering the mainstream, the day isn’t far when people will be using blockchain-based wallets for making quick and safe transactions.

How Can Appventurez Help You in Business Transformation with Blockchain Development?

To get the best out of blockchain’s unique capabilities, it’s better to focus on the issues that it is best suited to resolve. For this, it becomes crucial to deploy blockchain technology in the best way possible.

Therefore, if you are also interested in understanding how to implement blockchain in business efficiently, the most important part is finding a professional blockchain app development company.

Appventurez is one of the leading software app development companies specializing in blockchain app development. The company has already delivered a plethora of blockchain-based solutions and is helping many other clients with their projects’ requirements. The development team at Appventurez is one of the early adopters of this disruptive technology, making it perfect as a collaborative partner for your next project.

![blockchain technology for business]()

FAQs

Q. How is the blockchain for businesses used?

With blockchain, businesses can quickly store, process, and transfer records with a robust in-built encryption mechanism to secure them from unauthorized access.

Q. How much does it cost a business to run a blockchain-based system?

The cost can range anywhere between $30,000 and $300,000. However, based on the type of features, technologies integrated, hourly charges of developers, and the location of a development company, the rates can vary.

Q. How long does it take to develop a blockchain?

Depending on the complexity of the blockchain solution, it can take anywhere around 2 to 8 months to build a blockchain.

Q. What are some popular examples of blockchain applications?

Some of the most popular examples of blockchain applications include smart contracts, wills and copyright protections, cryptocurrency, anti-money laundering, and blockchain-based advertising.

+1 424 -408-4326

+1 424 -408-4326 +44 7768229682

+44 7768229682 +91 9899650980

+91 9899650980