In the age of information and technology, the payment industry has undergone several transitions. The evolution of cashless payments, online wallets, and cryptocurrency has shifted the mode of transactions from traditional models to digital mediums by leaps and bounds. But why?

Well, quick fund transfer and ease of convenience are the two major possibilities. Today, one of the most important demands of a modern-day consumer is to get everything immediately with the least possible effort. In such a landscape, an efficient payment solution becomes crucial in order to provide them with the best experience possible.

The emergence of digital payment mediums has significantly held the share of spending through cash, cheques, and even cards. However, this ever-growing integration of digital payment technologies does raise a question: Are we set to accept and adopt these ‘digital-first’ modes of payment?

What Are Digital Payments?

Digital payments can be defined as the process of transferring money from a source account to the receiver’s account through a digital medium. Since the transactions are processed through online modes, the exchange of hard cash is not involved. That’s why digital payments are often known as e-payments (or electronic payments), too.

When a digital transaction is made, both the payer and payee need electronic mediums to make it happen. The payer uses any payment processing software or a digital device, say a smartphone or computer to initiate a transaction. Meanwhile, the financial services provider makes the digital bank transfer into the payee’s account in the backend.

Some popular types of digital payments include online bank transfers, cross-border transactions, mobile payments, and contactless payments.

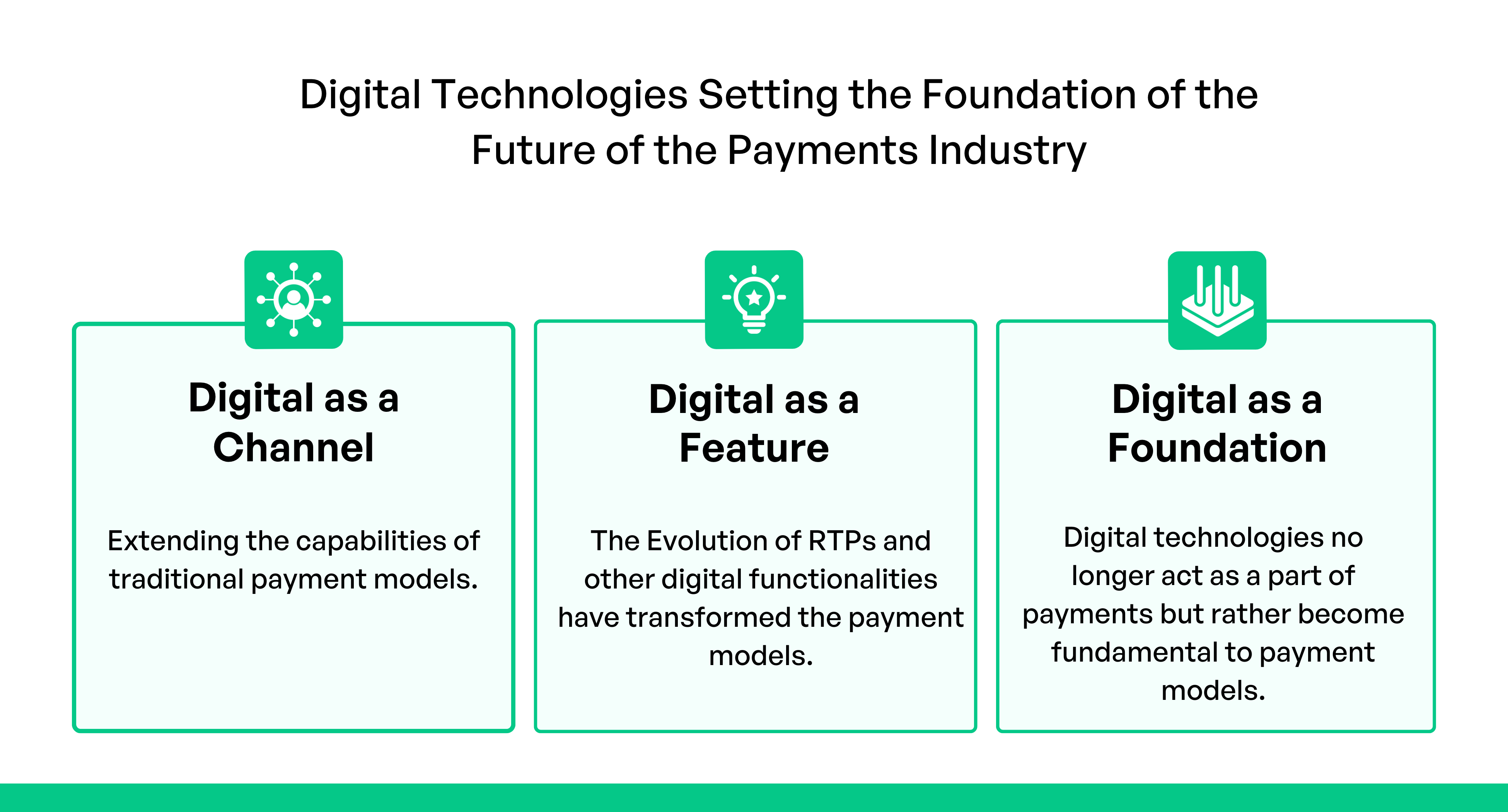

How Did Digital Payments Become Fundamental to Payment Models?

Initially, the incorporation of digital payment technologies was to extend the capabilities of traditional payment models. However, with the evolution of real-time payments (RTP), digital functionalities become one of the significant features of the transforming payment models.

Today, the increase in customer adoption of digital payments has made RTP an efficient payment solution, not only for peer-to-peer channels but also for B2B and B2C use cases. In addition, the impact of the pandemic also promoted cashless payment globally, which has replaced physical payment extensively.

![digital technologies are the foundation of future of payment industry]()

Besides this, improving traceability and accountability to ensure better user data security were also the primary concerns for the banking and financial sector. The significant features offered by digital payment technologies keep security intact and maintain a more efficient flow of economic resources, leading to seamless finance management.

Also, the emergence of newer innovations, such as blockchain technology and mobile payment mediums also became the new normal, gaining traction in the global marketplace. That’s why advancements in digital technologies are no longer just part of existing payment models but have become fundamental to them.

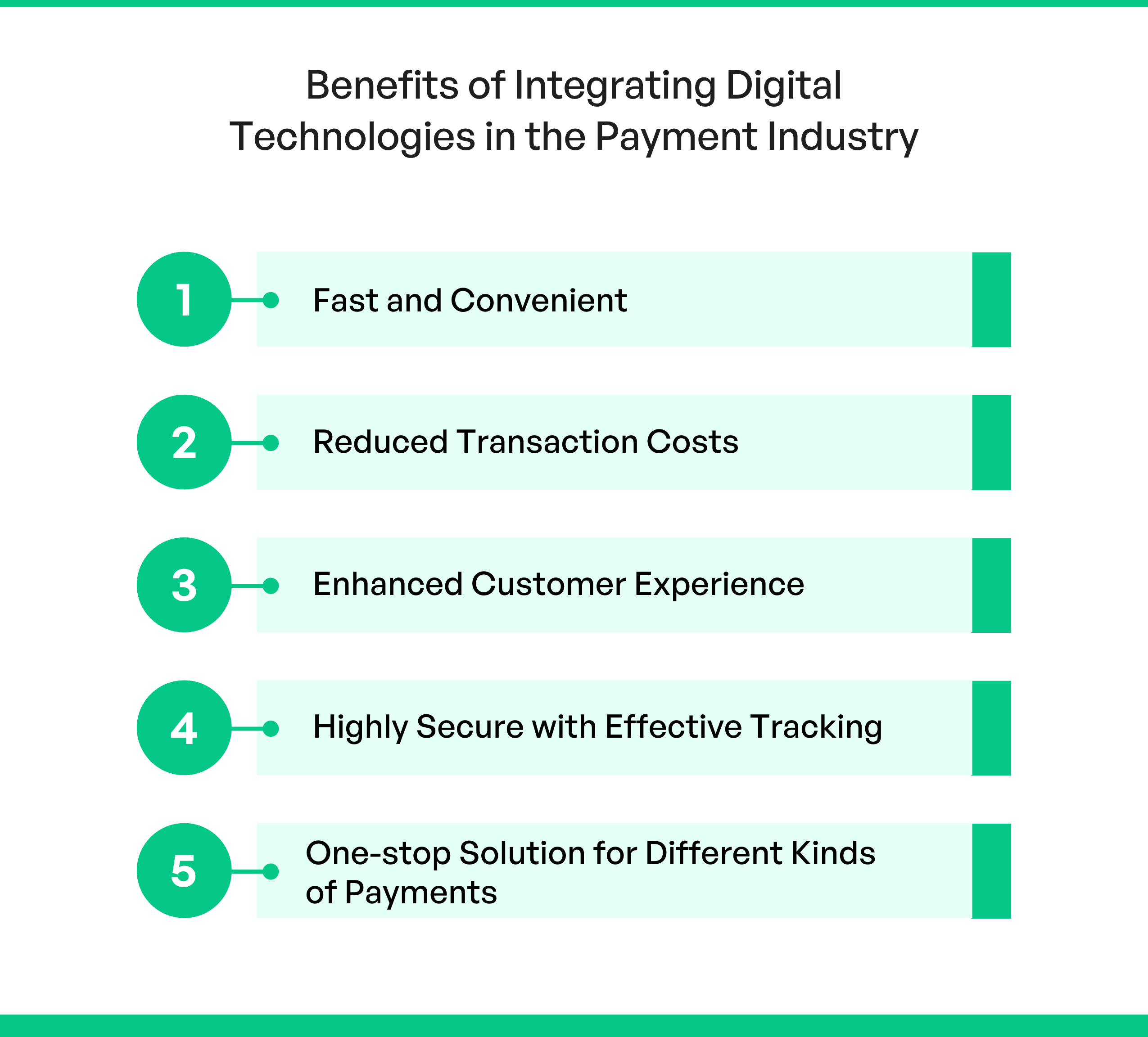

What Are the Benefits of Integrating Payment Technologies in the Industry?

To drive and maintain the global economy, it becomes necessary to have access to major financial resources, especially in developing countries. In such a context, technology plays a significant role by bridging the gap and building seamless fund transfer systems that are easily accessible through online applications.

In a digitized payment industry where the transaction value is all set to reach $9.47 trillion by this year, you can imagine how beneficial it could be for businesses.

![benefits of integrating digital technologies in payment industry]()

Quick, Easy, and More Convenient

One of the most significant benefits of digital payments, which might also be the reason for its inception, is convenience. Customers no longer have to worry about filling up long forms in a bank or standing in a queue outside ATMs to withdraw cash. Just a few taps on their mobile screen and they can easily share or receive payments in no time. Moreover, since everything is available to them through an online portal, they can easily avail of most banking services 24/7.

Economical with Negligible Transaction Fee

Earlier, large-scale businesses used to make over half of their payments through paper checks, while small-scale businesses preferred this medium for 80-90% of their transactions. These paper-based payments lead to a lot of hassle as collecting and processing paper checks are highly expensive and time-consuming. On average, it costs about $5 to process a single paper check and $13 just to share an invoice.

Besides the cost aspect, these paper-based payment methods are also slow. It can take up to two weeks to clear a check. On the contrary, paperless payment options are not only faster but comparatively cheaper. In fact, several payment portals and mobile wallets do not charge a single penny as a service charge, making the consumers transfer money free of cost.

Improved Customer Experience

Integrating new technologies in the payments sphere provides users with multiple payment options from which they can choose one as per their convenience. With digital payment channels, customers can avail of a self-service platform and transact anywhere worldwide under specific rules and regulations. When businesses offer them such fast, seamless, and convenient mediums, the customer experience naturally gets enhanced.

Effective Tracking Systems with High Security

One of the best things about digital payment solutions is that new payment methods are more secure than the traditional payment methods. Backed by several security methods, such as encryption, payment tokenization, SSL, etc., customers can easily transact across online channels without worrying about security aspects.

Furthermore, since all the transaction records are digitally maintained and encrypted, you get constant updates and digital statements to track them effortlessly.

One-stop Solution for All Kinds of Payments

Today, there are several payment-related applications offering multiple services through which consumers can pay different utility bills. It provides them with a one-stop solution for all their outstanding bill payments, be it electricity, phone, Wi-Fi, etc.

How Can Integrating Technological Solutions Impact the Future Growth of Payment Companies?

The emergence of digital payment solutions is not only impacting the industry but the growth opportunities for payment companies, as well. Here are a few points that help understand how incorporating digital solutions can explore future growth for payment companies.

Improving the Scope for Cross-Border Payments and Mobile Remittance

Over the years, the number of migrant workers is increasing significantly, especially in developing countries. Since sending remittances to their families back to their homes is common, a fast and convenient mode of payment can help them extensively. In such a case, developing cross-border and mobile remittance platforms can widen the scope of growth for companies in the payment industry.

Building Efficient Solutions for Underdeveloped Segments

In ASEAN (Association of Southeast Asian Nations) countries, over 60% of the population is rural or lives in rural areas. For the people living in those areas, accessing online modes of payment is still far from their reach. Creating immersive and convenient digital payment platforms for such untapped segments can be profitable for the population belonging to it. Therefore, when companies strive to expand their services in these areas, the more they can scale their business.

The Growth of Virtual Debit/Credit Card Payment Solutions

E-wallets or digital wallets have become one of the most common and widely used media of payments lately due to the convenience it offers to users. These wallets are linked with the user’s debit or credit cards and allow them to make transactions, but virtually, using QR codes and biometrics. Since these digital solutions offer both comfort and security, the implementation of these solutions is expected to grow more rapidly in the coming years.

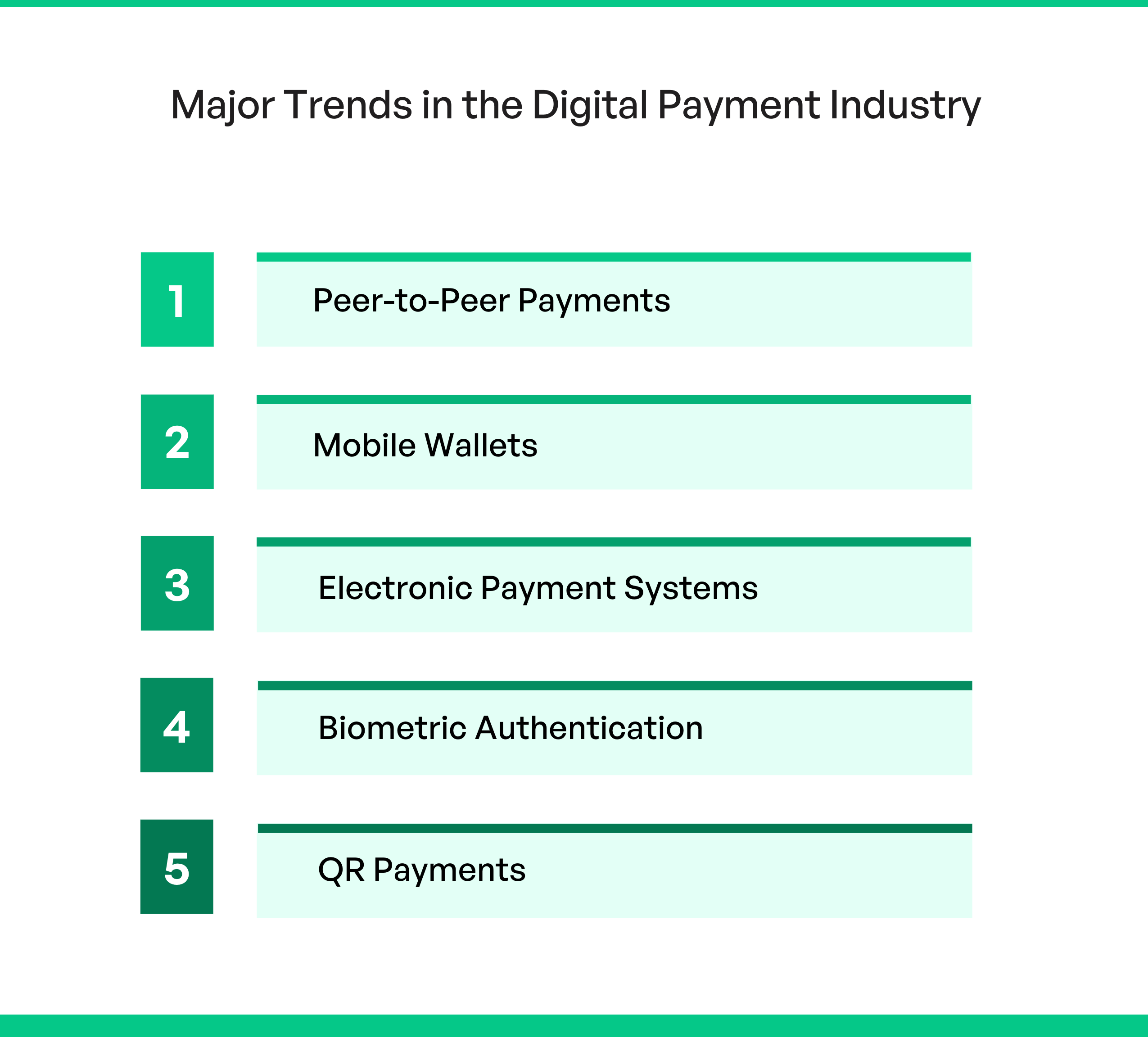

Major Payment Industry Trends Transforming the Payment Gateway

Implementing next-gen technologies in transferring money is becoming the new normal, especially after the fintech app development firms that build business across owning customer relationships. Several instances of technological advancements, such as the development of NFC banking apps, magnetic secure transmission, and digital currencies improved customer experience extensively while ensuring greater fraud detection.

As the digital payment industry moves in an upward trajectory, it becomes crucial to understand how technology has changed money and the mode of transactions. Here are the latest payment industry trends that businesses need to be updated about:

![major trends in digital payment industry]()

Peer-to-Peer Payments

Peer-to-Peer (or P2P) mode of payment involves an electronic medium through which one person transfers money to another person through an intermediary application. The funds are transferred using an online app or medium through the respective bank accounts or the credit cards of the people making the transaction. Venmo, PayPal, Apple Cash, etc. are some of the popular P2P payment apps.

Advancing P2P mobile payments will improve the opportunities for businesses to monetize their products and services extensively. In fact, it is also reported that the global P2P payment market size is estimated to touch the 9.1 trillion mark by the year 2030.

Mobile Wallets

Mobile wallets are similar to real wallets but in a digital form. Like you keep the wallets in your pockets or bags, these digital wallets are installed in smart devices, such as mobile phones or tablets. These digital wallets have become a fine replacement for swiping or inserting cards or keeping hard cash in your pockets.

Consumers often prefer this mode of online payments technology for its payment security and fraud prevention services. Some of the popular examples of mobile wallets are Google Pay, Apple Pay, and PayPal Wallet. The recent trends in digital wallets include the development of Bitcoin wallet solutions, the integration of QR codes for quick payments, and NFC-based technologies.

Electronic Payment Systems

The continuous adoption of online shopping practices has accelerated the growth of digital payment solutions, as well. Consequently, electronic payment systems have become the most popular mode of payment, especially in the eCommerce industry.

This immense popularity has forced stakeholders and business owners to reevaluate their payment strategies and integrate online payment solutions for customers’ convenience. Some common but widely used electronic payment systems include:

- Buy Now, Pay Later (BNPL) Solutions

It is a type of financing that allows customers to buy a product or service and pay later for the same over time, generally without any interest. This technique is often used by businesses to engage customers and enhance brand loyalty.

Electronic checks are the digital version of paper checks. eChecks use the Automated Clearing House (ACH) technique and a payment processing gateway to transfer money from a customer’s checking account into the merchant’s business account.

Biometric Authentication

Biometric authentication is a method through which your payment system or device verifies a person through any of their distinguishable biological traits, such as retina scans, fingerprints, or voice recognition. In the financial domain, biometric verification is done by mobile payment apps and other digital payment solutions to authenticate transactions.

For instance, when users make a transaction, the mobile payment solutions they are using share information about it along with a payment request on their devices. If enabled, the system will also ask for behavioral biometric information, successfully submission of which completes the transaction. This additional security layer makes the transaction process more robust and secure.

QR Payments

The evolution of QR-based payment solutions opened the doors to digital transformation in the payment industry by providing a faster, simpler, and safer payment medium to customers. Its easy-to-use approach makes it one of the most popular modes of digital payments in the current landscape.

In order to make a QR-based payment, all users have to do is open their bank’s app or any digital wallet and scan the QR code of the merchant. They have to select any digital payment method, like a card, net banking, or Unified Payment Interface (UPI) to process and complete the transaction.

![want to learn how mobile payments trends transform the future of the payment industry]()

Some New Technologies That Reshape the Payment Industry

Today, most advanced payment processing services involve the integration of artificial intelligence and machine learning. As consumers leverage digital payment gateways to make a transaction, the ML algorithms analyze their data and purchase behavior that businesses can use later to improve customer experience.

Moreover, this user data can also be saved with users’ permissions to provide faster solutions the next time users make a purchase through the same medium. Also, along with improved customer experience, the integration of new technologies in the payment domain ensures a great level of security. Some of the prominent technologies used by payment industry companies are:

Open-Banking APIs

Using open banking application programming interfaces, legacy banks can easily transfer data among each other with the help of third-party apps. Basically, these APIs are used by any B2B or B2C company to incorporate their products and services into a non-financial company’s platform.

Based on the services customers use, open banking providers can charge them and open new revenue streams. Moreover, they can also work with clients and gain insights that can be used to improve their services.

However, as of 2021, only 30% of financial institutions were using open-banking APIs. The reason behind this is that most of them were already coping with the challenges related to the older tech infrastructure.

Mobile Point of Sale

Mobile Point of Sale (or MPOS) is another popular technology that leads to digital transformation in the payments industry. It facilitates several mobile payment solutions in locations, such as parking lots, retail stores, hotels, etc.

For example, a mobile POS solution allows customers to pay from any location inside a departmental store without standing in a queue at billing counters. In a similar manner, hotel staff does not need to perform formalities at the front desk to check the visitors in or out. This mobile payment trend is not only used in stores or hotels but also by SMBs or even large organizations.

AI-based Voice Payments

After GPS navigation and mobile shopping, AI-based voice assistants are all set to help users with bill payments through an integrated voice-tracking system.

AI-based voice technology will be incorporated into payment apps, transforming the future of payment technology. With this, users can leverage the AI-powered smart speakers to pay the bills using a specific set of commands, making payments convenient and seamless. It is also reported that smart speakers can be the next big thing, changing how businesses interact with their consumers.

Distributed Ledger Technology

Several companies in the financial domain are now using distributed ledger technology (DLT) that removes the intervention of third parties from the core processes. Blockchain technology, perhaps the most popular DLT, is often used to create highly secure and tamper-proof logs of sensitive user data.

This technology builds user trust, ensures transparency, and reduces transaction costs and time. Besides this, blockchain also helps businesses in reducing the processing time from several days to a few hours, especially in the case of cross-border payments.

Internet of Payments (IoP)

Being one of the services of ever-growing IoT technology, the Internet of Payments revolutionizes the banking and financial sector significantly. IoP allows fintech companies to process transactions over IoT devices, such as wearables or smart automobiles.

For example, FitBit Pay, one of the features in a FitBit band, offers users to make contactless payments using tokenization. Similarly, consumers can use in-car payment apps to pay seamlessly at gas stations and parking lots – thanks to IoT transforming the automotive industry.

What is the Future of Digital Payments?

The global payments industry is at its tipping point. The emergence of the fintech revolution has unlocked the doors to a new sphere where the way transactions take place is no longer the same.

On the one hand, where digital payment solutions are paving inroads into the financial market, transactions through hard cash and cards on the other find it challenging to stay relevant. To hold their place in the market, even the cards and banking network is striving hard to reshape the payment experience for users.

By seeking technological assistance, the payment industry is building a personalized connection with customers. The key focus is on incorporating low-cost high-volume P2P payment mediums and e-commerce and m-commerce channels. By strategically leveraging digital technologies and developing their core strengths, businesses can easily offer compelling and competing payment solutions prepared for the modern audience.

How Appventurez Can Help Businesses Build Robust Digital Payment Solutions?

In the present fast-moving landscape, maintaining and enhancing customer satisfaction levels has become one of the top-most priorities for businesses. Since the availability of different payment options is a crucial aspect in enhancing the customer experience, businesses must adopt next-gen technologies to gain a competitive edge.

Since the future of payment technologies seems bright, having an immersive digital payment solution that processes transactions faster and offers a secure platform to consumers could be profitable. However, for this, businesses need a professional finance app development company that has expertise in different digital payment technologies.

Appventurez specializes in creating fintech apps that provide users with a powerful platform where they can easily access flexible payment processing services. Our experts are well-versed in all the major state-of-the-art technologies needed to integrate an ideal fintech solution into your business model.

![looking for a robust fintech app development solution]()

FAQs

Q. What are payment gateways?

A payment gateway can be defined as a payment processing technology used by stores and merchants to accept eCommerce, POS payments, and debit or credit card purchases from consumers.

Q. What are digital wallets?

A digital wallet or e-wallet is a financial software program or online payment service that enables businesses or individuals to make transactions. A person needs to install these digital wallets on their mobile phones or computer systems and link their financial accounts in order to make payments.

Q. Are contactless payments safe?

Contactless payments are way faster, safer, and more convenient than card payments. With contactless payment options, the data is transmitted to the POS device instantly in an encrypted form, making it highly secure from cybercriminal activities.

Q. How technology has reshaped the payments industry?

Consumers on a global scale looked for efficient contactless payment solutions, especially after the pandemic. New and robust technologies in the payment industry bridged that gap by developing instant, seamless, and feasible online payment solutions. By incorporating digital technologies like mobile wallets, QR payments, and biometric authentication, making transactions become fast, convenient, and cost-effective.

+1 424 -408-4326

+1 424 -408-4326 +44 7768229682

+44 7768229682 +91 9899650980

+91 9899650980